TL;DR: Between 2023 and 2025, Austin added more new apartment units than almost any city in America, over 60,000 across the metro. As of early 2026, roughly 10,000-13,000 additional units are still scheduled for delivery this year. That wave is slowing fast. Construction starts hit a ten-year low in 2024, which means the oversupply window — and the concessions that come with it — has a shelf life.

We track Austin’s apartment inventory daily across 1,000+ properties through our custom search tool. So when we say the development pipeline is shifting, we’re watching it happen in real time, community by community, corridor by corridor.

Here’s what most “new apartments in Austin” articles get wrong: they list buildings. That’s it. A name, an address, maybe a rendering. What they don’t tell you is what all that new supply actually means for your rent, your negotiating power, and your timeline.

This guide is different. It’s a data-driven tracker of what’s being built, where, how many units, and when those units will deliver. We also break down what that supply means for pricing, where the pipeline has gaps, and how renters can use delivery schedules strategically to get better deals.

The sources behind this data include RentCafe, CoStar, RealPage Analytics, the Austin Apartment Association, Cushman & Wakefield, Yardi Matrix, the City of Austin Housing Department, and the Downtown Austin Alliance, all cross-referenced against our own database. Where projections differ between sources (and they do), we note the range.

Austin’s Construction Numbers in Context

To understand what’s being built now, you need to understand what just happened.

Austin went on a building spree between 2021 and 2024 unlike anything the city had seen. Developers launched a record number of projects between 2021 and 2023, riding pandemic-era migration, cheap capital, and job growth forecasts that wouldn’t quit. Construction timelines of 18-36 months meant those units started flooding the market in 2023 and 2024.

| Year | Approx. Units Delivered (Metro) | Construction Starts Trend | Source |

|---|---|---|---|

| 2022 | ~18,000 | Peak year for new starts | RentCafe / CoStar |

| 2023 | ~25,000 | Starts declined 43% from peak | MMG Real Estate Advisors |

| 2024 | ~33,000 | Starts declined another 60%, hitting a ten-year low | CoStar / RentCafe |

| 2025 | ~26,715 (metro) / ~15,195 (city) | Pipeline still delivering prior starts | RentCafe |

| 2026 (projected) | 4,600 – 13,000 | Dramatic drop as prior starts run dry | CoStar / RealPage / AAA |

The numbers tell a clear story. Deliveries peaked in 2024. They’re already declining. By 2026, the metro could deliver as few as 4,600 new units according to CoStar’s latest estimates, a 74% drop from the roughly 17,500 delivered in 2025. RealPage puts it higher at around 10,300 units for 2026, and the and the Austin Apartment Association cites 12,000-13,000. The exact number depends on how you define the metro boundary and which delayed projects actually finish on schedule.

But every source agrees on the direction: sharply down.

That’s the headline renters need to understand. The construction wave is not building — it’s receding.

Austin’s population grew 10.9% from 2020 to 2024, the fastest-growing large metro in the country. Tech jobs, in-migration from higher-cost states, and a growing remote-work population all fueled that growth. And that growth prompted the record development starts. Those projects are now delivering, even as new starts have dropped off a cliff.

What’s Delivering and Where: Corridor-by-Corridor Breakdown Since March 2026

Not all submarkets received new supply equally. Some corridors absorbed thousands of units over the past two years. Others barely saw a crane.

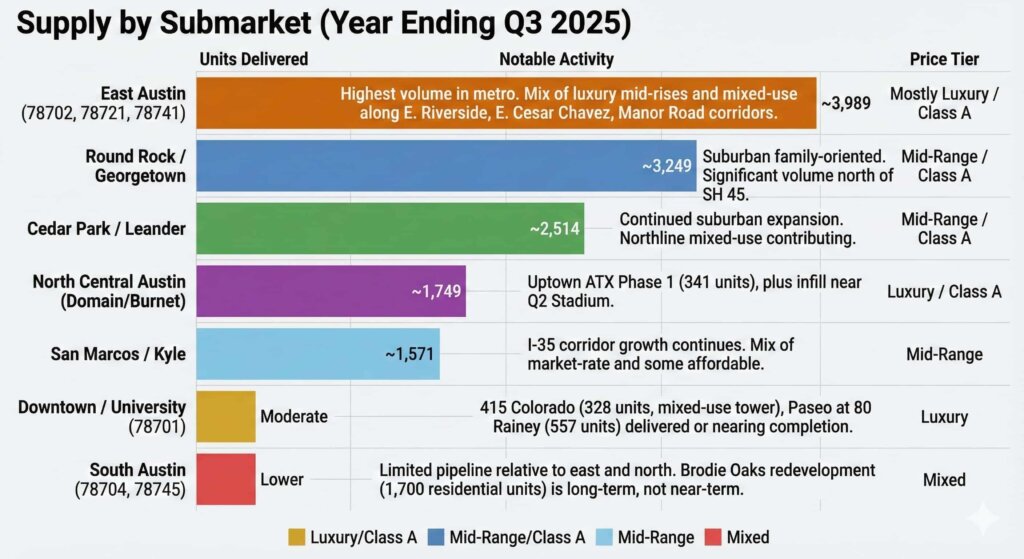

Based on RealPage data through Q3 2025 and our own database tracking, here’s where the heaviest delivery activity concentrated:

Supply by Submarket (Year Ending Q3 2025)

| Submarket / Corridor | Units Delivered | Notable Activity | Price Tier |

|---|---|---|---|

| East Austin (78702, 78721, 78741) | ~3,989 | Highest volume in metro. Mix of luxury mid-rises and mixed-use along E. Riverside, E. Cesar Chavez, Manor Road corridors | Mostly Luxury / Class A |

| Round Rock / Georgetown | ~3,249 | Suburban family-oriented. Significant volume north of SH 45 | Mid-Range / Class A |

| Cedar Park / Leander | ~2,514 | Continued suburban expansion. Northline mixed-use contributing | Mid-Range / Class A |

| North Central Austin (Domain/Burnet) | ~1,749 | Uptown ATX Phase 1 (341 units), plus infill near Q2 Stadium | Luxury / Class A |

| San Marcos / Kyle | ~1,571 | I-35 corridor growth continues. Mix of market-rate and some affordable | Mid-Range |

| Downtown / University (78701) | Moderate | 415 Colorado (328 units, mixed-use tower), Paseo at 80 Rainey (557 units) delivered or nearing completion | Luxury |

| South Austin (78704, 78745) | Lower | Limited pipeline relative to east and north. Brodie Oaks redevelopment (1,700 residential units) is long-term, not near-term | Mixed |

Source: RealPage Analytics (October 2025), supplemented by individual project tracking.

A few things jump out from this data.

East Austin absorbed the most units by a wide margin. Nearly 4,000 in a single year. That kind of supply dump in one submarket is why concessions along East Riverside and the Plaza Saltillo corridor have been among the most aggressive in the city. Zip code 78741 alone added 6,459 apartments over the past decade, and 78702 added another 6,067.

Downtown delivery has been notable but more constrained by land availability and construction costs. The projects that did deliver are large-scale towers (415 Colorado, Paseo on Rainey) that add density to an already tight footprint.

The suburbs (Round Rock, Cedar Park, Georgetown) continued steady output, mainly targeting renters priced out of central Austin or commuting to employers like Dell, Apple, and Samsung.

Major Active and Recently Delivered Projects by Corridor

We can’t verify delivery dates for every project in the pipeline (some shift quarterly), so the table below focuses on named projects we can confirm through public records, developer announcements, or our database. We’ll update this section as timelines firm up.

Downtown / Rainey Street

| Development | Developer | Location | Units | Delivery Status | Price Tier |

|---|---|---|---|---|---|

| 415 Colorado | Lincoln Property Co. / Kairoi | 415 Colorado St (78701) | 328 (apartments) | Delivered 2025 | Luxury |

| Paseo | Aspen Heights / Pappageorge Haymes | 80 Rainey St (78701) | 557 | Late 2025 / Early 2026 | Luxury |

| The Modern Austin | Kairoi Residential | Rainey St (78701) | 365 | Delivered Q1 2025 | Luxury |

| Waterline | Lincoln Property Co. | Congress Ave bridge area | 352 (in mixed-use tower) | Projected 2026 | Luxury |

Downtown’s pipeline is dominated by luxury high-rises. Base rents for 1-bedrooms in these towers typically start at $2,200-$3,000+ before concessions. But with multiple towers delivering in the same window, concessions of 6-10 weeks free have been common — which drops net effective rent by $1,100-$2,500 over a 12-month lease. If you’re looking at downtown Austin apartments, the concession environment right now is stronger than anything we’ve tracked since 2020.

East Austin / East Riverside / Plaza Saltillo

| Development | Developer / Manager | Location | Units | Delivery Status | Price Tier |

|---|---|---|---|---|---|

| Eastpoint | Various | Near Airport Blvd (78702) | ~300+ | Delivered 2024 | Class A |

| Nexus East | Greystar | E. 7th St area (78702) | ~280 | Delivered 2021 | Class A |

| River Park (Phase 1) | Presidium / Partners Group | E. Riverside at Pleasant Valley | 5,000 (full buildout, phased) | Phase 1 delivering; full buildout TBD | Luxury / Mixed |

| Multiple mid-rises along E. Riverside | Various | East Riverside corridor (78741) | 2,000+ (aggregate) | Various 2024-2025 | Luxury / Class A |

East Austin has been the single biggest recipient of new construction in the city. The East Austin apartment market looks nothing like it did three years ago. Thousands of new units have come online along East Riverside, East Cesar Chavez, and the Manor Road corridor. The River Park project alone, when fully built out, will add 5,000 multifamily units. That’s a phased development happening over many years, but the scale gives you a sense of where this corridor is headed.

Right now, competition between new buildings here is fierce. We’re tracking concessions of 2-3 months free across multiple East Austin communities, and some properties along East Riverside are running even deeper specials to fill up.

North Burnet / Domain Area

| Development | Developer | Location | Units | Delivery Status | Price Tier |

|---|---|---|---|---|---|

| Uptown ATX (One Uptown) | Brandywine Realty Trust | 11501 Burnet Rd | 341 (Phase 1) | Delivered 2024 | Luxury |

| Uptown ATX (future phases) | Brandywine | North Burnet corridor | 2,000+ (multi-phase) | Phased through 2030+ | Luxury / Class A |

| Lenox Burnet | Various | Burnet Rd corridor | ~350 | Delivered/Leasing 2025 | Class A |

| Broadstone North Lamar | Alliance Residential | North Lamar (78758) | ~300 | Leasing 2025 | Class A |

The North Burnet / Domain corridor has loose zoning compared to most of Austin, which is why it keeps attracting development. Uptown ATX — the $3 billion, 66-acre redevelopment of the former IBM campus — is the biggest single project in this area. It’ll eventually include a new CapMetro MetroRail station along the Red Line. Phase 1 is done. Future phases will roll out for years. If you’re exploring the north Austin apartment market, this corridor has some of the newest inventory in the metro.

Concession examples in this corridor as of early 2026: Lenox Burnet (315 units, built 2024 at 6801 Burnet Rd) was offering 2 months free on 12-month leases with 1-bedroom base rents starting at $1,234. Broadstone North Lamar (298 units at 6709 N. Lamar) had studios from $1,490 with leasing incentives during its initial fill. These deals shift month to month, but the pattern is consistent: newer properties in this corridor are competing hard for tenants.

South Austin / South Lamar / South Congress

| Development | Developer | Location | Units | Delivery Status | Price Tier |

|---|---|---|---|---|---|

| Brodie Oaks Redevelopment | Barshop & Oles / Lionstone | South Lamar at Loop 360 | 1,700 (full buildout) | Long-term; phased TBD | Mixed |

| The Prescott | Richman Signature | 8200 S Congress Ave (78745) | 348 | Delivered 2022 | Luxury |

| Various infill projects | Multiple | South Lamar corridor | Several hundred aggregate | 2024-2025 | Class A / Luxury |

South Austin’s pipeline has been more modest compared to the east and north sides. The Brodie Oaks redevelopment, a 37.6-acre mixed-use project at South Lamar and Loop 360, will eventually add 1,700 residential units. But that’s a long-horizon project that won’t move the needle on supply in 2026. Near-term, the south side has fewer new deliveries, which is one reason occupancy in South Austin held up better than most submarkets (above 94% as of October 2025, per RealPage).

Concessions exist in South Austin but aren’t as deep as East Austin or the Domain because supply pressure is lower here. Mueller, the master-planned community on the old airport site, is essentially built out for multifamily rental, so don’t expect new supply there either.

What All This New Supply Means for Renters

Here’s where the data gets practical.

When thousands of apartment units deliver in a condensed window (which is exactly what happened in Austin from 2023 through 2025), the market tips in renters’ favor. Properties compete for the same pool of tenants. That competition shows up as concessions.

As of 2025, CoStar tracked that 65% of complexes in Austin were offering some type of concession. A separate Apartment List analysis from October 2025 found that 50% of Austin properties were offering concessions equivalent to at least one month’s free rent, up from 41% just a year earlier. That number was much lower in 2021-2022, when vacancy sat below 4%.

Common concessions in the current market:

- 4-12 weeks free rent on 12-14 month leases

- Waived application fees (typically $50-$150 per applicant)

- Reduced or waived administrative fees ($100-$400 savings)

- Reduced security deposits

- Look-and-lease bonuses ($250-$1,000 for signing quickly after touring)

- Some properties have offered up to 3-6 months free on select units

How to translate concessions into actual savings using net effective rent:

A new luxury 1-bedroom advertising $2,200/month with 8 weeks free on a 12-month lease:

$2,200 × 10 months paid ÷ 12 months total = $1,833 net effective rent

That’s $367/month less than the advertised price, totaling $4,400 over the life of the lease. Our custom search tool ranks properties by net effective rent (actual cost after concessions) rather than advertised rent, which is how sites like Zillow and Apartments.com sort results.

We break down this math in detail in our apartment pricing guide. It’s the single most important calculation renters overlook.

If you want to reach out directly, give us a call at 512-360-0852 and we can walk through which new construction communities currently have the deepest concessions in your target area.

The catch renters should know: Concessions typically apply to your first lease term only. Year-two renewal typically jumps back to the full base rent — and often increases 5-12% on top of that. A property offering 2 months free might increase rent 8-12% at renewal. So a new luxury building with big upfront concessions might actually cost more over 24 months than a Class A property with a stable rent structure and no concessions.

What’s NOT Being Built: The Affordable Housing Gap

The development pipeline tells you what’s coming online. It also tells you what’s missing.

The overwhelming majority of new construction in Austin is priced at the luxury or “luxury-lite” level. Of the 60,000+ units that delivered from 2023-2025, most fell into two buckets: Class A+ properties (built in the last 0-5 years, 1-bedroom rents starting at $1,800-$3,000+) or Class A properties ($1,500-$2,200 for a 1-bedroom).

Austin has made real progress on affordable housing. From 2020 to 2024, approximately 13,343 apartments were income-restricted in the city, making up about 14% of all new housing during that period, according to a RentCafe analysis. The city delivered 4,605 affordable units in 2024 alone, double the 2023 numbers, and Yardi Matrix projects 9,528 affordable units will deliver from 2025 to 2027 across the metro.

That progress is real. Austin had the third-highest rate of new affordable apartment construction in the country from 2020-2024, per RentCafe.

But the gap persists, particularly for deeply affordable units serving households earning 30% or less of area median income. The City of Austin’s 2017 Strategic Housing Blueprint set a goal of adding 60,000 income-restricted units over ten years. Six years in, production was behind target, especially in central and western council districts. The city has approved over $88 million in combined AHFC funding for affordable developments in recent years (1,429 units from a $42 million package plus 728 units from a $46.1 million package). That’s significant money. But the pace of development hasn’t caught up to the scale of the need.

What this means practically: if you’re searching for apartments in the $800-$1,200/month range for a 1-bedroom, very little of the new construction pipeline targets your budget. The oversupply, and the concessions that come with it, is concentrated in the $1,500-$3,000+ range. Below that, inventory remains tight. You can search the City of Austin’s AHOST tool to find income-restricted properties, and review income and rent limits to see if you qualify.

If you’ve run into screening challenges (a broken lease, eviction history, or credit issues), new construction is rarely the answer. Those communities typically run the strictest screening. Our second chance apartments guide covers which properties work with less-than-perfect rental histories.

Some market-rate units have effectively filtered down to more moderate price points as landlords drop rents to compete with new supply. But “filtering” (where formerly market-rate units become more affordable over time) is an unpredictable process, and it doesn’t solve the structural gap for Austin’s lowest-income residents.

How to Use This Information: Timing Your Move Around Deliveries

If you have flexibility on when you sign a lease, you can use the development pipeline strategically.

The logic is simple: When a cluster of new buildings opens for leasing in your target area around the same time, competition for tenants intensifies. Properties (both the new ones trying to fill up and the existing ones trying to keep tenants) offer deeper concessions.

Practical application for 2026:

1. Know which corridors still have deliveries coming. East Austin, the Domain/North Burnet area, and Downtown still have projects completing this year. If you’re targeting those areas, you’ll have more negotiating power than in South Austin or Mueller, where the pipeline is thinner.

2. Time your lease to overlap with peak delivery periods. New buildings typically offer their deepest concessions during initial lease-up, the first 3-6 months they’re on the market. After that, as occupancy rises, the specials tighten.

3. Don’t ignore existing buildings. When a new luxury tower opens down the street, the 5-year-old Class A building next door often drops pricing or adds concessions to keep tenants from leaving. These “competitive response” deals can be some of the best value in the market — newer-ish property, discounted because it’s competing with the shiny new building down the block.

4. Factor in renewal economics. A new construction deal with 3 months free sounds great until renewal hits and your rent jumps 30%. If you plan to stay longer than one year, calculate the net effective rent across 24 months, not 12. The cheaper-looking new building might cost more over two years than the established property with steady pricing.

5. Use the shrinking pipeline to your advantage — now. Deliveries are dropping sharply in 2026. CoStar estimates just 4,600 new units. Market analysts project occupancy to tighten back toward the 95% “effectively full” mark by early 2027, and positive rent growth could resume by late 2026 or early 2027. The renter’s negotiating window is narrowing. If you’ve been thinking about upgrading or relocating within Austin, the next 6-12 months offer better conditions than what’s likely coming after.

For a personalized breakdown of which new construction communities in your target neighborhoods currently have the best concessions and availability, reach out to us at 512-360-0852 or start with our custom apartment search tool. It ranks every property by net effective rent so you can compare apples to apples.

What Nobody Tells You About Moving Into a Lease-Up

New construction concessions are real, and the savings can be significant. But moving into a building during its initial lease-up comes with trade-offs that listing sites and property marketing won’t mention. Here’s what to expect.

The amenities might not be ready. That rooftop pool in the rendering? The coworking lounge? The dog park? During lease-up, it’s common for amenities to open weeks or months after the first residents move in. Construction timelines slip, final inspections take longer than planned, and management prioritizes getting units move-in ready over finishing common areas. We’ve seen residents move into buildings where the fitness center didn’t open for 2-3 months after the first leases started. Ask the leasing team specifically which amenities are operational today versus projected.

Construction noise is part of the deal. If a building delivers in phases (and many of the larger Austin projects do), you may be living next to active construction on unfinished floors, adjacent buildings, or parking structures. River Park on East Riverside, for example, is a multi-phase project where early residents will share the site with ongoing construction for years. This isn’t a dealbreaker for everyone, but it’s worth asking: how many phases are left, what hours does construction run, and which side of the building faces the active work?

Punch list items are normal. New units often have minor defects: paint touch-ups, cabinet hardware that’s loose, a dishwasher that wasn’t connected properly, grout that needs resealing. Good management teams handle punch list items quickly. Less organized teams let them pile up for weeks. Check Google reviews for other lease-up properties by the same management company to see how they handle the first 6 months.

Staffing is still ramping up. New buildings sometimes open with a skeleton crew. Maintenance response times during the first few months can be slower than the property’s long-term standard. Package rooms may not be fully set up. Parking assignments might change as occupancy shifts. These are temporary growing pains, but they’re real.

The upside of lease-up timing: You get first pick of floor plans, preferred floors, and corner units. You lock in the deepest concessions the building will ever offer. And if you’re flexible on move-in dates, some properties will negotiate additional perks (a specific unit hold, waived pet deposits, or early access) during the initial fill.

The bottom line: lease-up deals are worth pursuing, but go in with clear expectations. Tour the actual unit you’ll be renting (not a model), ask which amenities are open now, and check the management company’s track record on other properties.

Frequently Asked Questions

How many new apartments are being built in Austin right now? The metro area delivered approximately 26,715 apartments in 2025, with Austin city proper accounting for about 15,195 of those units. For 2026, projections range from 4,600 (CoStar) to about 12,000-13,000 per the Austin Apartment Association, depending on how the metro boundary is drawn and whether delayed projects finish on schedule. Either way, it’s a significant decline from the 2024 peak.

Which Austin neighborhoods have the most new apartment construction? East Austin led all submarkets with roughly 3,989 units delivered in the year ending Q3 2025, followed by Round Rock/Georgetown (~3,249), Cedar Park (~2,514), and North Central Austin including the Domain area (~1,749). Downtown saw targeted high-rise deliveries, while South Austin had comparatively less new supply.

Are new apartment rents going down in Austin? Yes. Rents in Austin have declined approximately 20% from the August 2022 peak. CoStar estimates the average asking rent across the metro was about $1,525 as of Q1 2026. Year-over-year effective rents were down 3.9% through Q3 2025, according to Cushman & Wakefield.

Why are so many apartments being built in Austin? Short answer: population growth outran housing supply for years. Austin grew 10.9% from 2020 to 2024, faster than any other large metro. Tech hiring, in-migration from California, New York, and other expensive markets, and a growing remote-work population all drove that demand. Developers responded with a record number of starts between 2021 and 2023. Those projects are delivering now, even though new starts have cratered.

Will Austin apartment rents go back up? Probably, but not right away. CoStar forecasts that positive rent growth may not resume meaningfully until early 2027. For 2026, the market is still absorbing excess inventory from the 2023-2025 delivery flood. The good news: you still have time to lock in favorable terms before that window closes.

What does “net effective rent” mean on new construction apartments? Net effective rent is the actual monthly cost after concessions are prorated across the lease term. If a new building advertises $2,000/month with 2 months free on a 12-month lease, the net effective rent is $1,667/month ($2,000 × 10 ÷ 12). It’s a more accurate comparison tool than advertised rent, especially when new buildings compete with different concession structures. Our apartment pricing guide breaks down the full math, and our search tool at search.austinapartments.com ranks by net effective rent automatically.

Is there affordable housing being built in Austin? Yes, but not at the pace needed. About 14% of new housing built in Austin from 2020-2024 was income-restricted, amounting to 13,343 units. The City of Austin has committed over $88 million to affordable development projects. Yardi Matrix projects about 9,528 affordable multifamily units will deliver from 2025-2027. The structural gap is most acute for households earning 30% or less of area median income. Check the City of Austin’s AHOST tool to search income-restricted properties.

When is the best time to get a deal on a new apartment in Austin? Right now through late 2026. The oversupply from the 2023-2025 delivery wave has created a concession environment that won’t last forever. Deliveries are dropping sharply, and occupancy is expected to tighten toward 95% by early 2027. October through February typically offers the deepest seasonal concessions on top of the oversupply discounts already in play.

Should I wait for a specific new building to open? Maybe. If a building you like is 2-3 months from opening, the lease-up period offers the best concessions. But don’t wait indefinitely. New buildings fill their most desirable units first (higher floors, preferred layouts), and concessions tighten as occupancy rises above 80-85%. Once a building is stabilized (typically 90%+ occupied), the specials dry up.

What are the downsides of moving into a brand-new building? Amenities may not all be open yet, especially pools, fitness centers, and coworking spaces that require final inspections. If the building delivers in phases, expect construction noise from unfinished sections. Punch list issues (minor cosmetic defects, loose hardware, plumbing adjustments) are normal in new units. And staffing is often still ramping up, so maintenance response times during the first few months may be slower than the long-term standard. None of these are dealbreakers, but they’re worth knowing about before you sign.

What’s the vacancy rate in Austin apartments? Cushman & Wakefield reported Austin’s multifamily vacancy at 10.2% as of Q3 2025, well above the 5-7% range considered healthy. But that number is trending in the right direction. C&W’s national year-end report showed Austin vacancy declined roughly 170 basis points from its peak, one of the biggest improvements among major metros. RealPage reported overall metro occupancy at 92.7% as of October 2025. The market hasn’t fully rebalanced, but the worst of the oversupply pressure is easing.

The Market Outlook: What Comes Next

The numbers paint a clear picture. Austin went through the most aggressive apartment construction cycle in its history. That wave is winding down. Construction starts hit a ten-year low in 2024, under-construction inventory fell 55% year-over-year, and deliveries are projected to drop 60-74% from their peak.

Demand hasn’t gone away. Austin’s population keeps growing. Tesla, Samsung, Apple, Dell, and Amazon continue to anchor job creation across multiple corridors. That demand, combined with sharply reduced new supply, points toward a market that tightens over the next 12-18 months.

Renters who act during the current oversupply window (roughly now through late 2026) can lock in the best pricing and concession terms this market cycle will offer. Once occupancy tightens back toward 95%, the advantage shifts back to landlords.

Don’t overthink it. Know what’s being built in your target area, compare by net effective rent, and move when the numbers work for you.

Looking for new construction apartments in Austin with the best current concessions? We track pricing, availability, and specials across 1,000+ properties daily. Call us at 512-360-0852 or start with our custom apartment search. It’s free, it ranks by actual cost, and it takes about 60 seconds.

Market data reflects available information as of March 2026 and is subject to change. Rent ranges and delivery timelines are based on analysis of our database, publicly available industry data, and third-party sources including RentCafe, CoStar, RealPage, Yardi Matrix, and the Austin Apartment Association. Verify current pricing and availability directly with apartment communities. The Austin Apartment Team operates under Spirit Real Estate Group, LLC (Broker License #562021).

{kind=link}